Telematics car insurance is a motor insurance product that monitors your driving behaviour through smartphone sensors or a vehicle-mounted device, then prices your premium based on how you actually drive [1][2]. Safe drivers pay less at renewal. Risky drivers pay more. The system replaces demographic guesswork with measured performance – your driving data becomes the primary factor in what you pay.

Traditional car insurance calculates your premium from your age, postcode, vehicle group, and claims history. Those factors stay fixed for 12 months regardless of what you do on the road. Telematics adds a behavioural layer – the insurer tracks your acceleration, braking, cornering, speed, rest patterns, and phone use, then generates a driver rating that feeds directly into your renewal price.

The result is a pricing model that rewards skill rather than statistics. A 22-year-old who drives smoothly and obeys speed limits proves their safety through data. No waiting years for a clean no-claims record. A 35-year-old with a minor historical claim demonstrates that their current driving is low-risk. Both get a route to lower premiums that traditional insurance simply cannot offer.

How Does Telematics Car Insurance Work?

The way telematics car insurance works is by collecting continuous driving data from your smartphone's accelerometer, gyroscope, and GPS – or from a dedicated vehicle device – then transmitting that data to the insurer's platform, where an algorithm generates a driver rating that directly determines your renewal premium [1][2].

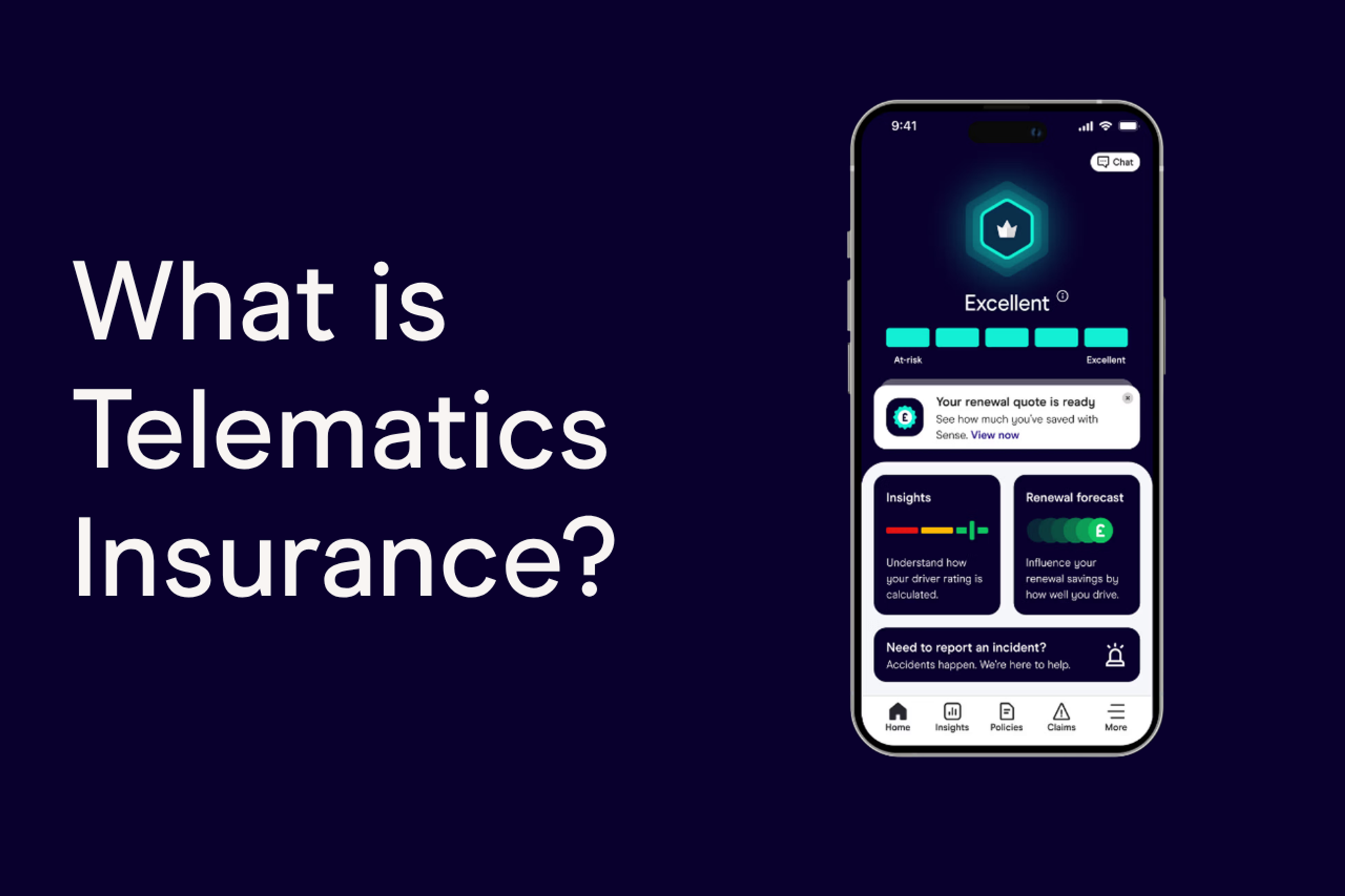

The data collection runs passively. Once you install the insurer's app or device, every journey is recorded without manual input. No buttons to press. No routes to log. The system measures 6 driving behaviours: acceleration smoothness, braking force, cornering control, speed limit compliance, rest between drives, and phone distraction.

Your score updates on a 28-day rolling average. One harsh braking event does not destroy your rating – consistent dangerous driving does. The rolling window rewards recent improvement, so drive safely this month and last month's mistakes begin falling out of the calculation.

At renewal, the insurer uses your accumulated score to set your new premium. Zego reports that 96% of Sense drivers paid less at renewal than their initial premium, based on data from June to August 2025. The core mechanism is direct: better data, lower price.

The insurer's underwriting team sees your aggregated score – not your raw GPS coordinates, specific routes, or individual journey details. What the underwriter receives is a risk number, not a surveillance file.

What Are the 2 Types of Telematics Car Insurance?

The 2 types of telematics car insurance in the UK are app-based telematics and hardware-based telematics, commonly called black box insurance [1][2]. Both monitor driving behaviour and generate a score, but they differ in hardware requirements, installation cost, and flexibility when switching vehicles.

App-Based Telematics

App-based telematics uses your smartphone's built-in sensors – accelerometer, gyroscope, GPS, and compass – to track driving behaviour. No hardware installation. No engineer visit. You download the insurer's app, grant the sensor permissions, and the system runs in the background from your first journey.

The sensors in a modern smartphone measure acceleration force, braking intensity, cornering angle, and speed relative to posted limits with sufficient accuracy for insurance scoring. Zego Sense is a fully app-based system that tracks all 6 driving metrics without requiring any device fitted to the vehicle.

The advantage is portability. Change your car and the app moves with your phone – no removal fee, no refitting appointment. The drawback is battery drain on longer journeys and the requirement to carry your phone in the vehicle on every trip.

Hardware-Based Telematics (Black Box)

Black box insurance fits a small device – roughly the size of a smartphone – into your vehicle's OBD-II diagnostic port or wired directly into the electrics. The device contains its own accelerometer, GPS receiver, and cellular modem. It draws power from the vehicle's battery, recording data even when your phone is dead or at home.

Installation requires either a professional appointment or a self-fit plug-in unit. Costs range from £50 to £100 for fitting, with additional removal charges when you switch vehicle or cancel [2]. That overhead is the trade-off for slightly higher data reliability in areas with poor mobile signal.

Black box policies dominated the UK telematics market between 2010 and 2020. App-based systems have overtaken them since 2021 as smartphone sensor accuracy improved and drivers rejected the friction of hardware installation [1].

Our full comparison of telematics vs black box insurance breaks down the cost and data differences in detail.

Who Is Telematics Car Insurance For?

Telematics car insurance serves drivers across all age groups in the UK, but the largest premium savings go to drivers aged 17–25 – the bracket where traditional insurance pricing is highest and the gap between demographic-based and behaviour-based premiums is widest [1][3].

Drivers aged 17–25 face the steepest traditional premiums – the average comprehensive policy for 17–19-year-olds costs £2,712 [3]. Telematics provides a route out of that bracket by proving driving skill through data rather than waiting years for a clean claims record. Premiums for the under-25 group average £1,450 on traditional policies but £980 on telematics – a 32% reduction [1]. The savings narrow as drivers age because traditional premiums fall, but telematics remains valuable for anyone who drives safely and wants their premium to reflect that rather than their postcode or birth year.

Zego Sense covers drivers aged 25–60 with no previous claims or motoring convictions, driving vehicles valued under £30,000 for social, domestic, and pleasure use. This is a specific eligibility window – younger drivers and those with claims history need different providers.

How Much Does Telematics Car Insurance Cost?

As a rough average the cost of telematics car insurance ranges between £460 and £1,313 per year in the UK, depending on age, driving behaviour, vehicle group, and postcode [1][3]. Safe drivers who maintain strong driving scores pay less at renewal than they would on a standard policy, with reported market savings of 20–40% [1][2].

The price at quote stage uses the same underwriting factors as any car insurance policy – age, postcode, vehicle group, and claims history. The difference arrives after you start driving. Your insurer tracks your behaviour, generates a score, and adjusts your renewal price based on real performance data rather than demographic assumptions.

For drivers aged 17–19, the average telematics premium is £1,313 compared to £2,712 on traditional cover – a gap of £1,399 [3]. For drivers aged 25–34, the gap narrows to around £130 [1]. The youngest drivers capture the largest savings because their traditional premiums carry the most uncertainty loading.

These figures are based on published UK market research and aggregated industry data from the Association of British Insurers, Insurance Times, and comparison platforms. Your actual premium varies based on your individual profile and driving behaviour – the numbers above represent market averages, not specific quotes from any single provider.

Zego Sense annual premiums start from £578.51, a figure representing the 10th percentile of customers in the six months prior to October 2025.

What Does Telematics Car Insurance Cover?

Telematics car insurance provides fully comprehensive cover – the same protection as any standard UK comprehensive policy [2][4]. The telematics element affects how the premium is calculated, not what the policy covers or excludes.

Standard inclusions on a comprehensive telematics policy: third-party liability, personal accident cover, windscreen repair and replacement, key and lock replacement, courtesy vehicle during approved repairs, and personal belongings protection. Optional extras vary by provider – Zego Sense offers breakdown cover at £34.99 per year.

The only operational difference between a telematics policy and a non-telematics policy is the requirement to use the app or device throughout the policy term. Your claims process, excess structure, and policy terms remain identical. Telematics monitors your driving. It does not change what happens when you need to make a claim.

Is Telematics Car Insurance Worth It?

Telematics car insurance is worth it for safe, consistent drivers, particularly those under 25, where the premium gap between telematics and traditional cover is widest [1][3]. The financial case weakens for older drivers with already-low premiums, where the percentage saving narrows to single digits.

The strongest argument for telematics is the renewal trajectory. Drivers who maintain high scores see their premiums fall year on year as the insurer accumulates behavioural data and reduces the uncertainty in their risk model. Traditional insurance reprices you annually against your demographic group. Telematics reprices you against your own record.

The trade-off is data sharing. Telematics requires you to let your insurer access driving data. The app tracks your journeys. Your acceleration, braking, cornering, and speed are scored continuously. For drivers who value privacy above cost savings, this exchange may not suit them. For drivers who want their premium to reflect actual behaviour rather than their age bracket, it is the most direct route available.

Our full guide to whether telematics insurance is cheaper covers the cost comparison between telematics and standard policies.

How Does Zego Sense Telematics Work?

The Zego Sense app-based telematics product tracks driving behaviour across 6 metrics – acceleration, braking, cornering, speeding, rest, and phone distraction – and generates a driver rating that directly determines your renewal premium.

Zego Sense eligibility requires drivers to be aged 25–60, hold a full or provisional UK driving licence, have no previous claims or motoring convictions, and drive a vehicle valued under £30,000 for social, domestic, and pleasure use.

The app runs in the background on your smartphone during every journey. It distinguishes automatically between driver and passenger, so only your driving is recorded. No manual input required. The phone's sensors capture your driving events and transmit the data to Zego's platform in real time.

Your driver rating is calculated as a 28-day rolling average across all 6 metrics. The rating activates after a minimum of 5 trips covering at least 65 miles. Once active, it updates daily and feeds directly into your renewal price.

Phone distraction is the newest metric, introduced in March 2026. The system detects when your phone is being held or interacted with while driving and adjusts your score accordingly.

At renewal, 96% of Sense drivers paid less than their initial premium, based on data tracked between June and August 2025. The Sense app provides real-time feedback on your score with detailed breakdowns of which behaviours affect it most. The underwriter sees your price adjustment but not your raw driving data – your routes, locations, and individual journey details remain private.

How Does Telematics Data Improve Insurance Pricing?

Telematics data shifts insurance pricing from demographic-based models – where age, postcode, and vehicle group set the premium – to behaviour-based models where actual driving performance determines the price [1][2]. This rewards safe drivers and penalises risky drivers more accurately than traditional actuarial methods achieve.

In traditional insurance, a 22-year-old in London pays roughly £1,400 per year because statistically, drivers in that demographic cause more claims [1]. Some of those drivers are exceptionally safe. Some are reckless. The insurer cannot tell them apart without years of claims data to work from.

Telematics resolves this within 28 days. The insurer measures actual behaviour – acceleration patterns, braking habits, speed compliance – and assigns a risk score grounded in observed data. A 22-year-old who drives smoothly and respects speed limits proves their safety immediately, earning discounts that would take years to achieve through a traditional no-claims bonus path.

Over time, telematics data also sharpens the insurer's actuarial models. Analysing millions of driving events across hundreds of thousands of policyholders reveals which specific behaviours predict claims with the highest accuracy. The scoring algorithm improves with each policy year. The result is a market where premiums increasingly reflect individual behaviour rather than group averages – and that benefits every driver whose skill exceeds what their demographic profile suggests.

Frequently Asked Questions

Does Telematics Car Insurance Affect Other Insurance Policies?

Your telematics driving score does not affect your home, life, or travel insurance. The score is proprietary to your motor insurer and used exclusively for car insurance premium calculation [2]. If your telematics insurer reports serious driving violations to the DVLA, the resulting record could affect future insurance applications across policy types – but this applies only to extreme cases and is rare in practice.

Can You Switch Telematics Insurers and Keep Your Driving Score?

Your telematics driving score is proprietary to each insurer and does not transfer between companies [2]. Each insurer uses a different algorithm, weights the 6 metrics differently, and defines risk thresholds independently. Switching means starting a new baseline with a fresh assessment period. The driving habits transfer naturally – safe behaviour generates a comparable score with any provider.

Is Telematics Data Shared With Police or Authorities?

Telematics insurers in the UK do not routinely share driving data with police or the DVLA. Insurers reserve the right to report evidence of extreme driving violations – sustained speeds well above legal limits, for example – but routine data on braking, cornering, and minor speed variations stays within the insurance relationship. Your policy documents specify the conditions under which data may be disclosed.

What Happens to Your Premium If Your Driving Score Drops?

A declining driving score affects your renewal premium, not your mid-policy price. Most telematics insurers hold your premium steady during the policy term and adjust at renewal based on your accumulated score. If your score drops due to increased harsh braking, speeding, or phone distraction, your renewal quote reflects that – either a flat premium with no discount, or a higher renewal price where the deterioration is significant.

References

[1] Association of British Insurers, "Three Straight Quarters of Falling Motor Premiums", November 2025. abi.org.uk (https://www.abi.org.uk/news/news-articles/2025/11/three-straight-quarters-of-falling-motor-premiums/)

[2] Confused.com, "Telematics Insurance Explained", 2026. confused.com (https://www.confused.com/compare-car-insurance/black-box/telematics-explained)

[3] Insurance Times, "Average price gap of £2,172 turns 83% of young drivers to telematics policies", 2024. insurancetimes.co.uk (https://www.insurancetimes.co.uk/news/average-price-gap-of-2172-turns-83-of-young-drivers-to-telematics-policies/1457022.article)

[4] WeCovr, "Telematics UK Insurance Costs 2026", March 2026. wecovr.com (https://wecovr.com/guides/telematics-uk-insurance-costs/)